SecondMarket™

Powered By Nasdaq Private Market

An institutional-grade trading platform to buy and sell blocks of private company stock.

Buy + Sell Stockeast

Software to Scale the Private Market

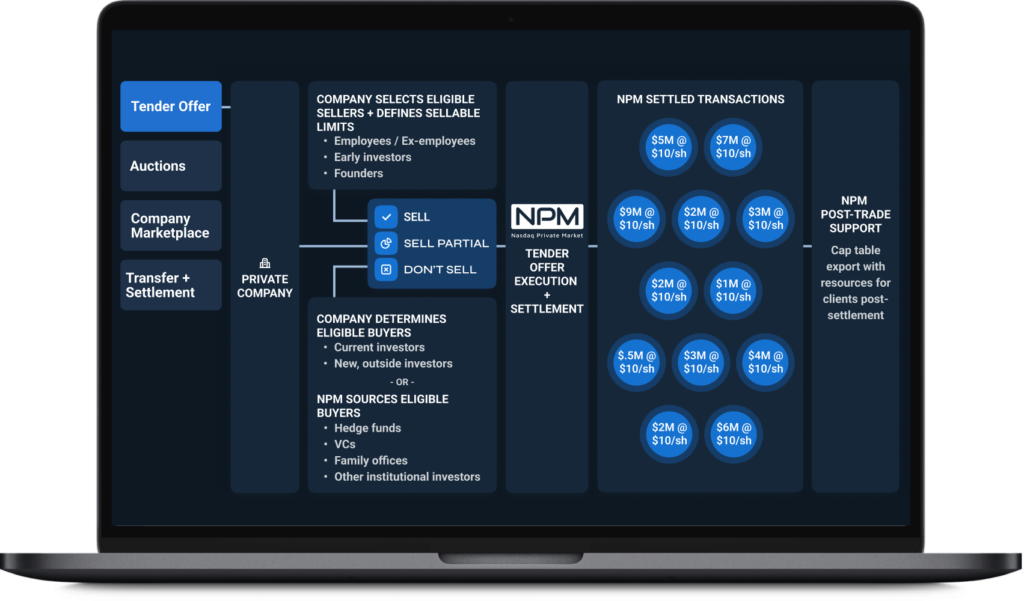

Transact with Confidence via One Global Platform

Whether you are a private market expert or new to secondary liquidity, let our product specialists help you navigate the secondary market and execute block trades.

Via our intuitive technology and experienced team, we guide you throughout the onboarding, execution, and settlement process making it as seamless as possible.

Our Trading Capabilities

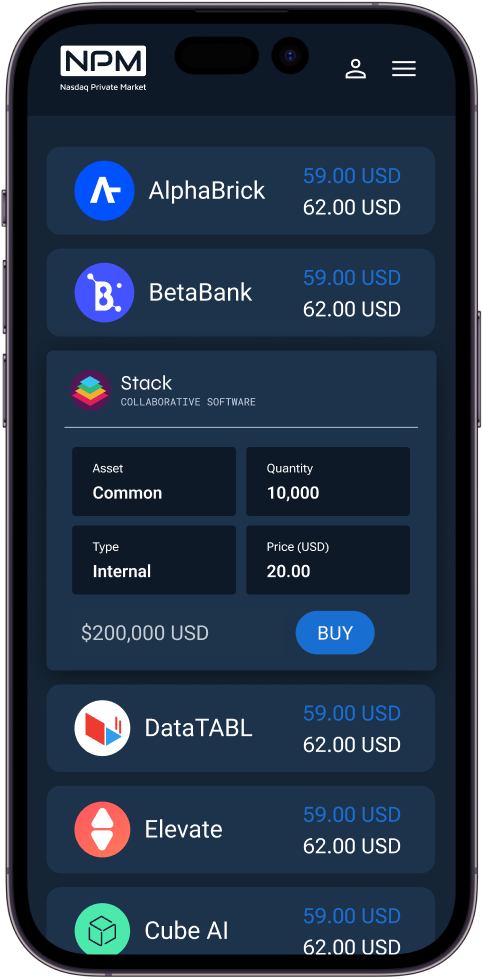

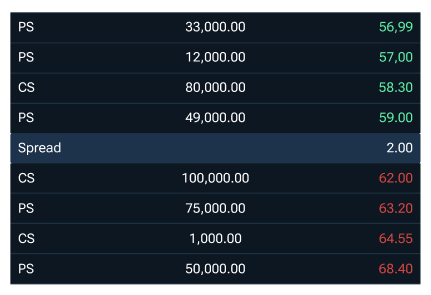

Buy + Sell StockeastAlternative Trading System

Order book, OMS, and crossing network for vetted members to trade private company shares.

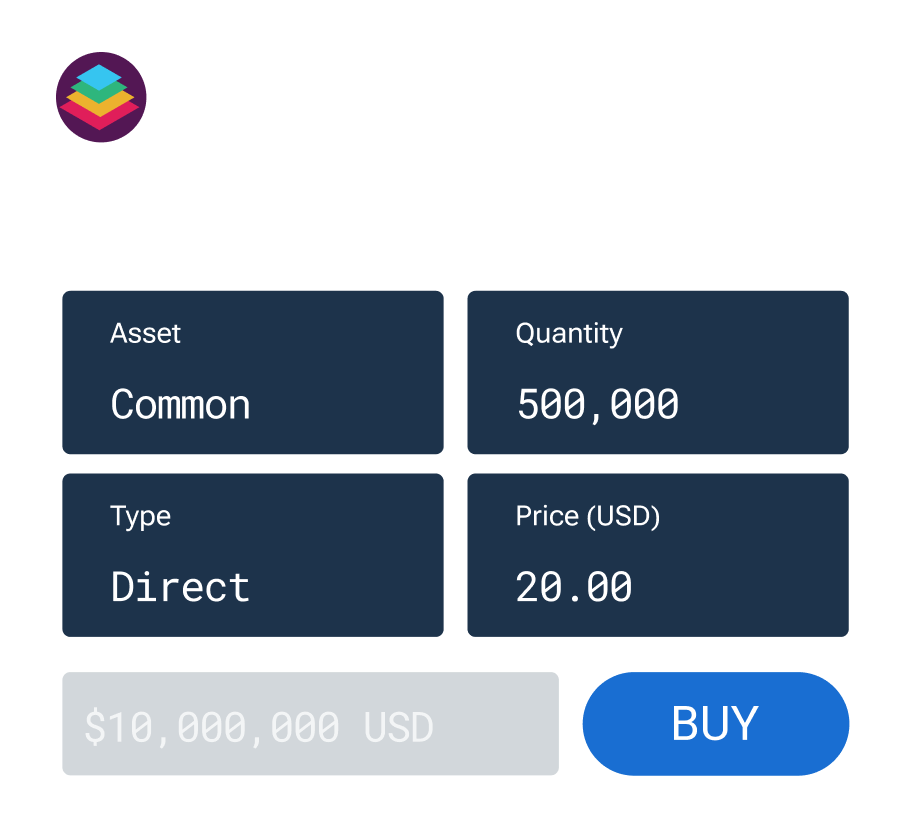

Customizable Trading Platform

Our end-to-end execution tools enable clients to set broker and investor workstations to meet their needs.

Negotiation Tracker

Simplify trade management with a centralized dashboard for accepting, countering, or rejecting offers from a wide network of participants.

Settlement

Streamline share transfers in one unified workstation, enhancing efficiency by structuring trade data to simplify the settlement process.

Onboarding

Get personalized support to get started and access SecondMarketTM features and functionality, unlocking your secure private company marketplace.

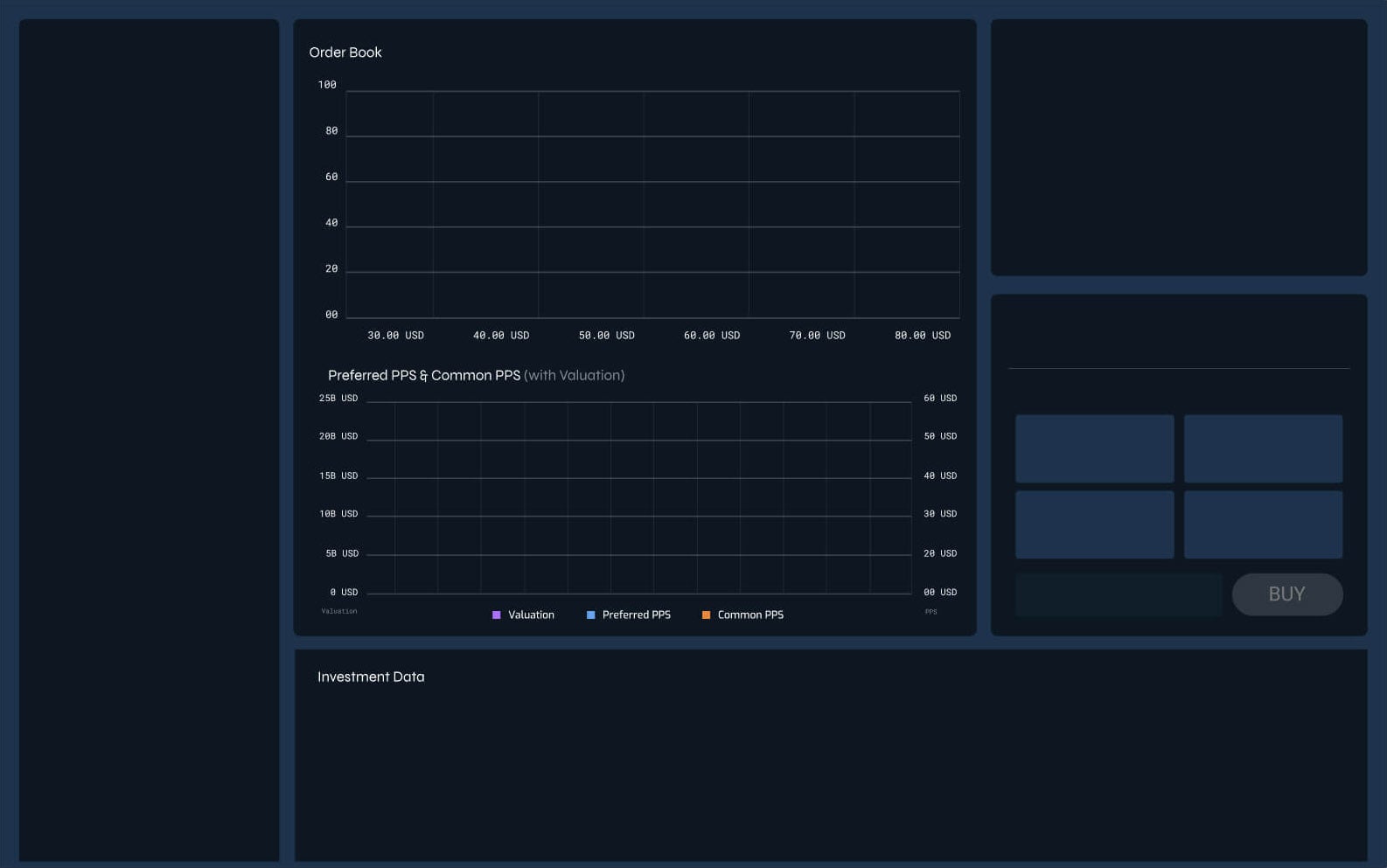

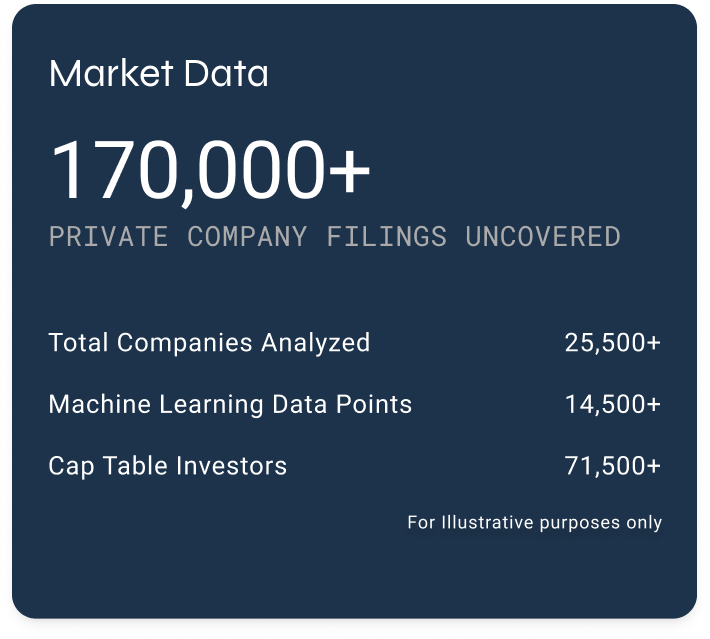

Market Data

Embedded proprietary finanacial products, data room, and private company ticker functionality to inform trading decisions.

A Platform Built With And For The Industry

Buy + Sell Private Company Shares

Comprehensive private market trading platform and suite of tools designed for efficiency and automation.

Compliant Infrastructure for Secondary Trading

Operating environment built to the needs of banks, brokers, and investors at each stage of a trade.

Analytics + Financial Data For Decision-Makers

Uncovering hard-to-source private company financials, valuation data, and other key company fundamentals.

Contract Management

Smooth transfer of shareholder documentation from sellers to buyers for transparency and record-keeping.

A Decade of Private Market Experience

Expertise

Private market pioneers and practitioners helping employees, shareholders, investors, banks, and brokers trade with proficiency in a new asset class.

Premier Global Network

Connect to Unicorn and high-value private company shareholders, active institutional investors, brokers, and banks worldwide.

Easy-to-Use Technology

Our frictionless platform has been built to the requirements of traders and investors with direct feedback from banks, brokers, and institutional investors.

Total Transaction Value

0

-

Total Company-Sponsored Programs

0

-

Number of Eligible Program Participants

0

-

Private Companies' Data Tracked

0

-

Onboarded Institutional Investors

0

-

Total Number of Unicorn Clients

0

Data as of January 2024

Thanks to Nasdaq Private Market we were able to offer eligible Docker employees valuable liquidity for their equity grants. Their commitment to client success continues to deliver powerful results for our team, shareholders, and investors.

Working with NPM, especially their tireless and service-oriented operations team, made our transaction a smooth one. NPM's support enabled us to keep our attention on the athletes we serve & employees who obsess over them.

NPM has been a key partner in Hopper's program to create multiple opportunities for partial employee liquidity. We appreciate NPM's creativity in adapting to Hopper's unique transaction structures.

NPM serves as an incredible partner for us. We’ve leveraged their secondary solutions multiple times to provide liquidity for employees. They deliver a professional and seamless experience for our team.

We had the pleasure of using the NPM platform and had a fantastic overall experience. Nasdaq Private Market’s knowledgeable and efficient team enabled us to successfully launch in a tight time frame.

Thank you to Nasdaq Private market for being a great partner throughout the tender offer process!